Over the past decade, the education sector has emerged as an attractive sector for private investment. Long-run global M&A deal volumes, compared to 2011, have grown faster in education than the general market (97% vs 28%). Deal volumes remain strong with 843 education deals completed in the last 12 months, tracking pre-Covid levels, despite economic uncertainty and high interest rates, which have affected all sectors.

From 2017 on, deal volume has been driven by PE firms and PE-backed companies acquiring companies to add on to existing investments. These PE add-ons have far outpaced both traditional PE and corporate-backed strategic deals.

The EdTech sector has been particularly volatile as Covid-driven digitisation of education and training drew massive investor interest, followed by a dramatic cooling off as valuations sky-rocketed and high-profile businesses struggled to compete in an increasingly crowded space (e.g. 2U which filed for bankruptcy and only recently emerged from its financial restructuring). In the past 12 months, assets have been coming to market but we have observed a number of EdTech deals being postponed due to mismatched buyer/seller valuation expectations.

However, there are signs of renewed investor interest in EdTech, as illustrated by a series of take-private deals (Kahoot!, PowerSchool, Instructure, Learning Technologies Group). One common motivation behind these deals and others is, perhaps, the imperative to internationalise. At Cairneagle, we note that our strategic clients are increasingly focused on internationalisation, often achieved through astute M&A.

Asia has seen the highest growth since 2011 yet remains a relatively small portion of deal volume.

Europe is the most active region for Education deals outgrowing the US. Western Europe accounts for nearly 80% of all European deals during the 2011-24 period. However, Southern Europe has seen fastest growth in deal volume through the end of 2023, overtaking Northern Europe for the first time in 2022 for the first time in terms and currently on track to do so again in 2024. Investors have been attracted to European education companies that have the potential to internationalise and grow with the appropriate investment. Benefitting from many of the same global drivers, we expect investment in European companies to continue to grow.

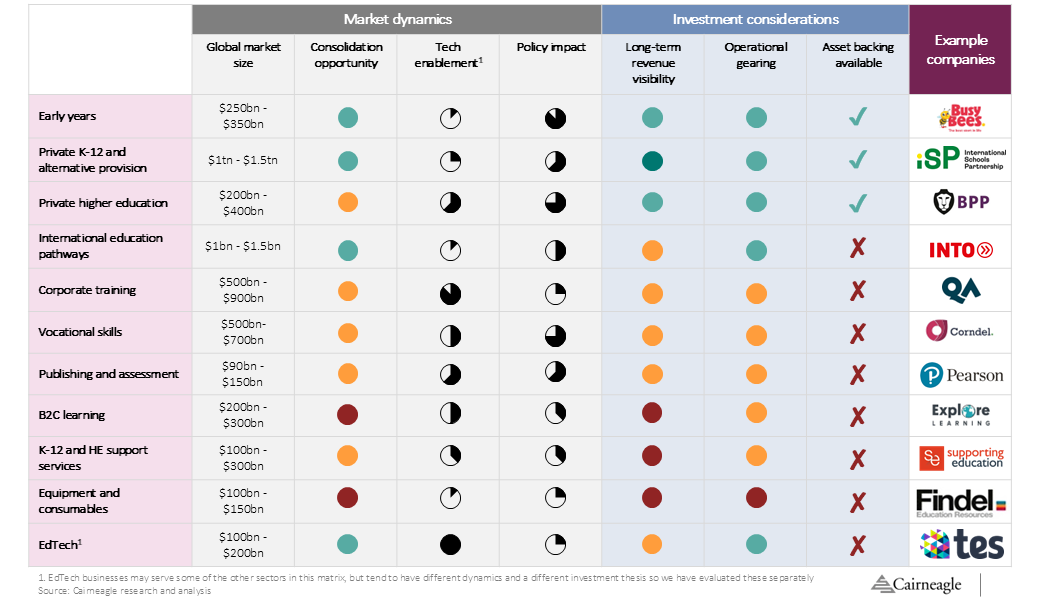

At Cairneagle, we are observing increasing levels of life and pipeline deal activity across the Education sector. There are attractive opportunities to fit with all different investment strategies across the various subsegments within education, as set out below.

If you are interested in discussing strategic or investment opportunities in Education, please get in touch.

Sam Lecacheur (Partner), Arun Kanwar (Partner), Jorge Amirola (Partner), Peter Friedman (Manager), Charlie Moore (Senior Consultant)

Footnotes: (1) 2024 data is year to date as of 1st October 2024.